A Complete Guide to SFC License Types and Exemptions

Operating in Hong Kong’s financial markets requires careful navigation of the Securities and Futures Commission (SFC) licensing regime. Whether you are a financial institution, fintech firm, asset manager, family office, or adviser, determining whether you need an SFC licence or registration is a threshold legal issue.

Hong Kong adopts an activity-based regulatory model under the Securities and Futures Ordinance (Cap. 571) (SFO). This means licensing obligations depend on what activities you conduct, not how your business is labelled

This guide provides a clear overview of the 13 SFC regulated activities, explains when an SFC licence or registration is required, outlines key licensing exemptions, and highlights common compliance risks across areas such as asset management, fintech, virtual assets, family offices, and cross-border operations.

Types of Regulated Activity Under the SFO

Schedule 5 to the Securities and Futures Ordinance (Cap. 571) (SFO) specifies 13 types of regulated activity, each with a detailed statutory definition. Carrying on any of these activities in Hong Kong—or actively marketing such services into Hong Kong—may trigger licensing or registration obligations.

The 13 SFC Regulated Activities

- Type 1 – Dealing in Securities

- Type 2 – Dealing in Futures Contracts

- Type 3 – Leveraged Foreign Exchange Trading

- Type 4 – Advising on Securities

- Type 5 – Advising on Futures Contracts

- Type 6 – Advising on Corporate Finance

- Type 7 – Providing Automated Trading Services (ATS)

- Type 8 – Securities Margin Financing

- Type 9 – Asset Management

- Type 10 – Providing Credit Rating Services

- *Type 11 – Dealing in or Advising on OTC Derivative Products

- *Type 12 – Providing Client Clearing Services for OTC Derivatives

- Type 13 – Providing Depositary Services for Relevant CISs

* Types 11 and 12 are not yet fully in operation for licensing purposes. In particular, Type 12 has only been partially brought into force since 1 September 2016, and this limited commencement relates solely to defining certain “excluded services,” rather than opening a full licensing regime. As a result, firms generally cannot apply for a standalone Type 12 licence at this stage. This does not mean that OTC derivatives or clearing-related activities are unregulated; instead, they may fall under other regulatory frameworks or transitional arrangements, and businesses should not assume that the absence of a full Type 12 regime removes compliance obligations.

The statutory definitions of each regulated activity are available in Schedule 5 to the SFO.

Do You Need an SFC Licence or Registration?

A critical compliance principle is that SFC licensing is determined by the activities actually carried on, not by job titles or business labels. Calling yourself a “consultant” does not avoid Type 4 (Advising on Securities). Managing client portfolios under a “family office” structure may still trigger Type 9 (Asset Management). Providing investment recommendations without executing trades can still require licensing. Additionally, marketing activities targeting Hong Kong investors can also trigger licensing, even if operations are offshore.

Business Activities That Trigger SFC Licensing Requirements

You are likely required to hold an SFC licence if you:

- Deal in or arrange securities or futures transactions

- Provide investment advice to clients

- Manage client assets on a discretionary basis

- Operate trading platforms or automated trading systems

- Advise on IPOs, listings, or takeovers

When an SFC Licence Is Required

Broadly speaking, you need an SFC licence if you are not an authorised financial institution and:

- You are a corporation carrying on a business in a regulated activity in Hong Kong;

- You actively market regulated services to the Hong Kong public, whether from within or outside Hong Kong;

- You are an individual performing a regulated function for a licensed corporation, in which case you must be a licensed representative, and possibly a responsible officer.

Sole proprietorships and partnerships are not acceptable business structures for SFC licensing purposes.

When SFC Registration Is Required

You need SFC registration, rather than a licence, if you are an authorised financial institution (e.g. a bank) and:

- You carry on regulated activities other than Type 3 (leveraged FX) and Type 8 (securities margin financing); or

- You actively market regulated services to the Hong Kong public.

Relevant individuals of registered institutions are not licensed by the SFC, but must be entered in the HKMA register. Licensed corporations and registered institutions are collectively referred to as “intermediaries.” Registration allows them to carry on regulated activities within the scope permitted by their banking licence.

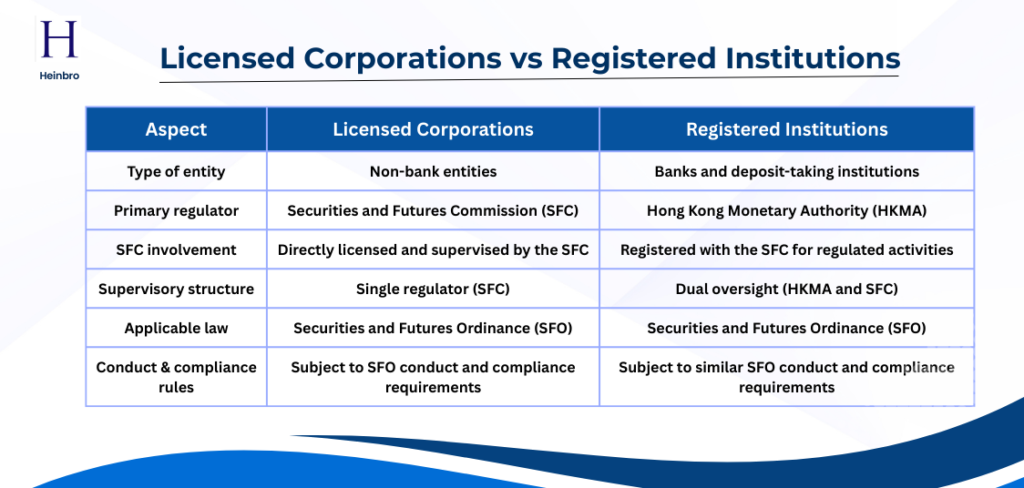

What’s the difference between Licensed Corporations and Registered Institutions?

Licensed Corporations are non-bank entities supervised by the SFC, while Registered Institutions are banks overseen by the HKMA and registered with the SFC, making them subject to dual regulation.

SFC Licence Exemptions

While the SFO offers certain licensing exemptions, these are narrowly applied and often misunderstood in practice.

Heinbro advises financial firms and institutions on SFC licensing and ongoing compliance. Where licensing or exemptions are uncertain, we conduct a careful, fact-specific review of your business model, transaction structure, and marketing activities. Book a free consultation at heinbro@heinbro.com.

1. Incidental Exemption

The incidental exemption applies where certain regulated activities are carried out wholly incidental to another regulated activity for which the corporation is already licensed.

In assessing whether this exemption applies, the SFC considers factors such as:

- Whether the activity is subordinate to the principal regulated activity

- Whether separate or discrete fees are charged

- Whether the activity constitutes a material or standalone part of the business

Type 1 Licence Holders Carrying Out Other Regulated Activities

A corporation licensed for Type 1 (Dealing in Securities) may not need separate licences for:

- Type 4 (Advising on Securities)

- Type 6 (Advising on Corporate Finance)

- Type 9 (Asset Management)

provided these activities are carried out wholly incidental to its securities dealing business. This exemption commonly applies to stockbrokers who provide investment advice or discretionary account management as ancillary services to securities dealing. However, it will generally not apply where discretionary asset management is offered as a distinct service and charged based on assets under management.

Type 2 Licence Holders Carrying Out Other Regulated Activities

A corporation licensed for Type 2 (Dealing in Futures Contracts) may rely on the incidental exemption for:

- Type 5 (Advising on Futures Contracts)

- Type 9 (Asset Management)

where such activities are subordinate to its futures dealing business. As with Type 1 scenarios, the exemption may fail if the services are structured or priced as standalone offerings.

Type 9 Licence Holders Carrying Out Other Regulated Activities

A corporation licensed for Type 9 (Asset Management) may carry out:

- Type 1 (Dealing in Securities)

- Type 2 (Dealing in Futures Contracts)

- Type 4 (Advising on Securities)

- Type 5 (Advising on Futures Contracts)

without additional licences, provided these activities are conducted solely for the purposes of managing portfolios under management. For advisory activities, this exemption applies only where the asset management involves a collective investment scheme. Placing trades or providing advice for portfolios not under management will generally fall outside this exemption.

2. Securities Dealer – Margin Financing Exemption

A corporation licensed for Type 1 (Dealing in Securities) does not need a separate Type 8 (Securities Margin Financing) licence to provide margin financing to its securities clients, provided it meets enhanced financial resources requirements, including higher paid-up capital thresholds.

This exemption typically applies to stockbrokers offering margin financing as part of their brokerage services. Authorised financial institutions are not required to be registered for Type 8 to carry out margin financing activities.

3. Credit Rating Services Exemption

A Type 10 (Providing Credit Rating Services) licence is required where credit ratings are prepared for public dissemination or subscription distribution.

However, licensing is generally not required where:

- Credit ratings are prepared solely for internal use, such as a bank’s internal risk assessment systems

- A firm only collects or disseminates credit information (not opinions) about entities other than individuals

- Consumer credit reference agencies are involved, as opinions on individuals’ creditworthiness are excluded from the statutory definition of credit ratings

4. Professional Investor Exemption

Licensing may not be required for dealing in securities or futures where a person acts solely as principal and deals exclusively with professional investors. This professional investor exemption may apply to futures contracts traded other than on a recognised futures market, as well as to securities dealings conducted only with professional investors. However, the exemption does not extend to intermediary or agency activities, and any person acting on behalf of others in such dealings will generally be required to hold the appropriate SFC licence.

5. Group Company Exemption

A corporation is not required to be licensed for Type 4, Type 5, Type 6, or Type 9 regulated activities where it provides advisory or asset management services solely within a wholly owned corporate group. However, this exemption is subject to important limitations: it does not apply where the advice relates to a group company’s client assets, and in the case of asset management, it applies only to the management of group assets, not third-party assets. Where a corporation manages assets belonging to clients of a group entity, this will generally constitute asset management and require a Type 9 SFC licence.

6. Professional Exemption

Solicitors, counsel, and professional accountants are not required to be licensed for Type 4, Type 5, Type 6, or Type 9 regulated activities where such services are provided wholly incidental to their professional practice. This exemption does not apply where regulated activities become a separate commercial service.

7. Broadcaster and Journalist Exemption

A person is not required to be licensed for Type 4 (Advising on Securities), Type 5 (Advising on Futures Contracts), or Type 6 (Advising on Corporate Finance) where investment advice, analyses, or related commentary are provided through publicly available media channels. This includes newspapers, magazines, books, or other publications made generally available to the public, as well as television or radio broadcasts accessible to the public, whether on a subscription basis or otherwise. This exemption is intended to cover general commentary and analysis, and does not extend to personalised investment advice or activities that otherwise constitute carrying on a regulated activity as a business.

8. Trust Company Exemption

In limited circumstances, a trust company may rely on exemptions from SFC licensing where regulated activities are carried out solely in the course of, and wholly incidental to, its duties as a trustee, rather than as a separate commercial business.

- Dealing in Securities: A trust company registered under Part VIII of the Trustee Ordinance does not require a Type 1 licence where it acts solely as an agent for a collective investment scheme to perform administrative or distribution functions.

- Investment Advisory Activities: No licence is required for Type 4, Type 5, Type 6, or Type 9 activities where advice or related services are provided wholly incidental to trustee duties and not offered as a separate advisory business.

- Asset Management Activities: A licence is generally not required where portfolio management is delegated to a third party or carried out based on professional advice; however, a Type 9 licence is required if the trust company itself conducts portfolio management as a standalone business.

9. Leveraged Foreign Exchange Trading Exemption

The SFO provides a number of exclusions in the definition of “leveraged foreign exchange trading”, meaning that not all such activities require an SFC licence. For example, authorised financial institutions, such as banks, are not required to be registered for Type 3 (Leveraged Foreign Exchange Trading) in order to carry out these activities. However, this exemption only applies where specific conditions are met.

SFC Licensing and Special Regulatory Scenarios

Certain business models, products, and operating arrangements raise additional SFC licensing considerations beyond the basic question of whether a regulated activity is carried on. The following guidance highlights common scenarios where firms frequently misunderstand their licensing obligations.

1. Conducting Regulated Activities Outside Hong Kong

An SFC licence authorises the holder to carry on regulated activities in Hong Kong only. Where a licensed corporation or individual conducts business activities outside Hong Kong, they must ensure compliance with the local laws and regulatory requirements of the overseas jurisdiction concerned.

Importantly, offshore operations do not automatically remove Hong Kong licensing obligations if activities are conducted in Hong Kong or actively marketed to Hong Kong investors. The SFC has issued guidance clarifying the licensing obligations of firms conducting cross-border business, and firms should carefully assess both Hong Kong and overseas regulatory exposure.

2. Financial Technology (Fintech)

Firms using innovative financial technologies to carry on regulated activities may apply to operate within the SFC Regulatory Sandbox. The Sandbox allows eligible firms to test regulated activities in a controlled environment, subject to additional licensing conditions, enhanced monitoring, and closer supervision by the SFC.

Participation in the Sandbox does not remove licensing requirements. Instead, it enables the SFC to impose tailored conditions to manage investor risk while innovation is tested.

3. Virtual Assets and Crypto-Related Activities

- Virtual Asset Fund Managers: Firms managing portfolios with more than 10% exposure to virtual assets are subject to additional regulatory standards imposed through licensing conditions. These conditions reflect heightened concerns around valuation, custody, liquidity, and investor protection.

- Virtual Asset Fund Distributors: Firms distributing funds that invest wholly or partially in virtual assets in Hong Kong are required to hold a Type 1 (Dealing in Securities) licence. The SFC has issued detailed guidance on expected standards and conduct when distributing virtual asset funds, reflecting the increased risks involved.

- Virtual Asset Trading Platforms: Centralised virtual asset trading platforms that offer trading in security tokens may apply for licences for Type 1 (Dealing in Securities) and Type 7 (Providing Automated Trading Services). This regulatory framework was introduced in 2019 and applies where at least one traded token is a security under Hong Kong law.

- Security Token Offerings: Security tokens are generally regarded as “securities” under the SFO. Unless an exemption applies, any person marketing or distributing security tokens—whether in Hong Kong or targeting Hong Kong investors—will require a Type 1 licence.

- Bitcoin Futures: Bitcoin futures traded on conventional exchanges are treated as futures contracts under the SFO. Parties dealing in such products as a business are therefore required to hold a Type 2 (Dealing in Futures Contracts) licence.

4. Online Financial Information and Tools

Providing financial information online does not usually require an SFC licence if the content is general and non-personalised. Generic factual market information and publicly available publications may rely on the periodical publication exemption, provided no investment recommendations are given. However, online tools that generate investment recommendations based on user-specific inputs may trigger Type 4 or Type 5 licensing requirements, whereas tools that simply filter publicly available data using objective criteria generally do not.

5. Financial Training and Educational Content

Providing general financial education or investment knowledge does not usually require an SFC licence. However, where training content moves beyond education and includes specific investment recommendations or inducements to trade, licensing obligations may arise for the institution, instructor, or platform operator.

6. Promotional and Incentive Schemes

Promotional schemes and referral arrangements present significant licensing risks. Paying commissions or incentives to unlicensed persons for introducing clients to licensed intermediaries is generally unacceptable and may expose both parties to regulatory liability. The SFC has consistently warned against structures that circumvent investor protection safeguards.

7. Private Equity, Venture Capital, and Fund-Related Activities

Private equity and venture capital activities may or may not require licensing depending on whether the underlying investments constitute “securities” under the SFO. While shares of Hong Kong private companies are excluded, investments in offshore private companies often fall within the securities definition, triggering licensing requirements.

As a general guide:

- Discretionary fund managers require a Type 9 licence

- Fund distributors or marketers may require Type 1 and/or Type 4 licences

8. Inter-Dealer Brokers

Inter-dealer brokers are commonly required to hold Type 1, Type 2, and/or Type 3 licences, depending on the instruments traded and booking arrangements. Exemptions may apply in limited circumstances, but most inter-dealer brokerage activities fall squarely within regulated activity definitions.

9. Investment-Linked Assurance Schemes (ILAS)

Insurers and insurance intermediaries dealing solely in ILAS products are generally not required to be licensed under the SFO. However, variations in product structure or distribution arrangements may give rise to licensing obligations.

10. Licensing of Compliance Officers and In-House Counsel

Back-office staff, including compliance officers and in-house legal counsel, are generally not required to be licensed unless they perform functions directly related to regulated activities. The SFC expects clear segregation between compliance/legal functions and regulated activity execution to avoid conflicts of interest.

11. Discretionary Investment Authority

To be licensed for Type 9 (Asset Management), a corporation is generally expected to exercise discretionary investment authority over client portfolios. Such authority must be properly delegated and documented.

12. Family Offices

The SFC’s licensing regime is activity-based, not structure-based. Single family offices managing only family assets and not providing services to third parties may not require licensing. However, family offices operating as businesses and managing assets that include securities or futures contracts often require a Type 9 licence, and potentially other licences depending on services provided.

13. Depositaries and Custodians of Funds

Depositaries of SFC-authorised collective investment schemes are generally required to be licensed or registered for Type 13 (Providing Depositary Services), subject to limited exemptions. Custodians of private Open-Ended Fund Companies (OFCs) must meet specific eligibility and financial resource requirements, and the SFC may impose additional licensing conditions.

Tips on SFC Licence Types and Regulated Activities

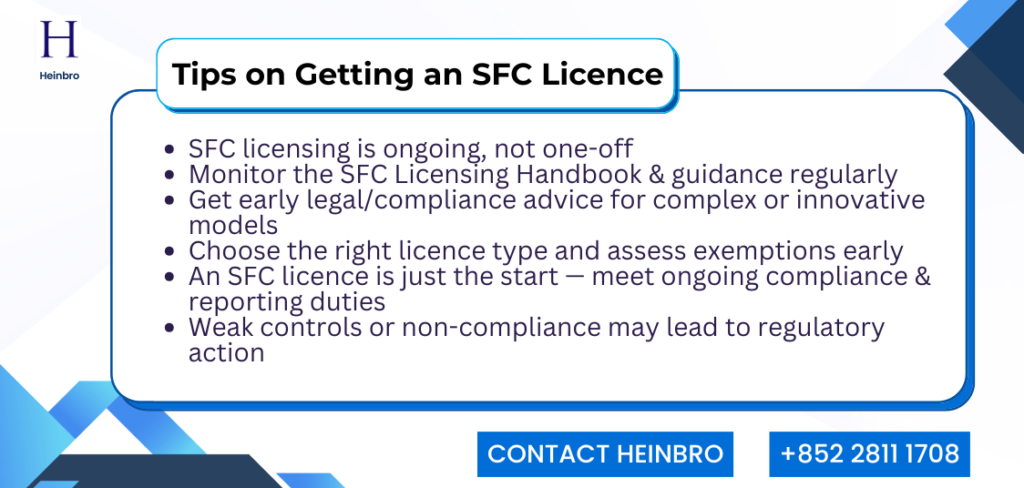

Understanding SFC licence types is not a one-off exercise. Firms operating in Hong Kong’s regulated financial markets are expected to take a proactive and ongoing approach to regulatory compliance, particularly as regulatory expectations continue to evolve.

- Refer to the SFC Licensing Handbook and Official Guidance: The SFC Licensing Handbook, together with circulars, guidelines, FAQs, and position papers, are essential references for understanding licensing requirements and regulatory expectations. These materials are updated regularly, and firms are expected to monitor changes and align their policies and operations accordingly.

- Seek Early Legal or Compliance Advice Where Needed: Early professional advice is critical where business models are complex, cross-border, or innovative, including fintech, virtual assets, algorithmic trading, fund structures, and family offices. Timely advice helps identify the correct licence types, assess the applicability of exemptions, and avoid structural or licensing issues that are difficult to correct later.

- Meet Ongoing Post-Licensing Obligations: Obtaining an SFC licence is only the first step. Licensed intermediaries must maintain adequate financial resources, comply with conduct, suitability, and disclosure requirements, implement effective internal controls and conflict management frameworks, and meet ongoing supervisory and regulatory reporting obligations. Failure to do so may result in regulatory action or licence restrictions.

Final Thought: Compliance Starts with Heinbro

Determining the correct SFC licence type and understanding when licensing exemptions may apply are critical compliance steps for any financial firm operating in or targeting Hong Kong. The SFC’s activity-based regulatory regime leaves little room for assumptions, and misinterpreting licensing obligations or exemptions can result in serious regulatory consequences. As business models become more complex—particularly in areas such as fintech, virtual assets, fund management, and family offices, professional guidance is essential to ensure compliance from the outset and to manage ongoing regulatory obligations effectively.

Heinbro provides specialised SFC licensing and ongoing compliance services to financial firms and institutions, supporting clients throughout the full regulatory lifecycle. From assessing licensing requirements and exemption applicability, to preparing licence applications, designing compliant operating structures, and advising on post-licensing obligations, Heinbro helps firms navigate the SFC regulatory framework with clarity and confidence. Get in touch with Heinbro at heinbro@heinbro.com, or call +852 2811 1708 to book a free consultation.