Hong Kong Private Trust Company Guide: Regulation, TCSP & Family Office Strategy

As wealth creation accelerates across Mainland China and Hong Kong, ultra-high-net-worth (UHNW) families are re-evaluating traditional offshore trust models. Increasing regulatory transparency, geopolitical considerations, and the desire for closer governance control have driven many Chinese entrepreneurs to consider establishing a Private Trust Company (PTC) in Hong Kong.

However, Hong Kong does not operate a standalone PTC regime like Cayman or BVI. Structuring a Hong Kong private trust company requires careful analysis of the TCSP licensing regime, AML compliance obligations, SFC regulatory exposure, and cross-border PRC risks.

This guide provides a 2026 legal and compliance-focused roadmap tailored specifically for Hong Kong and Mainland China UHNW families.

What Is a Private Trust Company (PTC)?

A private trust company (PTC) is a company established for the sole purpose of acting as trustee for a specific family’s trusts. Unlike commercial trust companies that serve the public, a PTC acts exclusively for a defined group—typically members of one family or related entities.

Legally, the PTC assumes the same fiduciary duties as any trustee:

- Duty of loyalty to beneficiaries

- Duty of prudent investment

- Duty to act in accordance with trust terms

- Duty to manage conflicts of interest

However, its governance structure allows families to participate directly in trustee-level decisions—an advantage rarely available with institutional trustees.

Core Structural Components of a Private Trust Company

A properly structured private trust company typically includes:

- The PTC Entity – Incorporated as a limited company.

- Board of Directors – Often includes family members and independent professionals.

- Shareholding Structure – Frequently owned by a purpose trust or foundation.

- Underlying Family Trusts – The PTC acts as trustee for these trusts.

Importantly, ownership of the PTC is often structured to avoid estate inclusion or personal liability exposure.

Common Ownership Models for a Private Trust Company

- Purpose Trust Ownership (Common Offshore Model)

A non-charitable purpose trust holds shares of the PTC. This structure is common in Cayman Islands and BVI to ensure neutrality and avoid direct family ownership. - Foundation Ownership

Civil law jurisdictions such as Panama or Liechtenstein may use a foundation to hold the PTC shares. - Family Holding Company Model

In some U.S. structures, a family-owned entity may hold shares, subject to tax and estate planning considerations.

Selecting the appropriate ownership structure requires coordination between legal, tax, and compliance advisors.

Are Private Trust Companies Regulated?

Regulation depends on jurisdiction. Broadly, PTC regimes fall into two categories:

- Regulated PTCs – Subject to licensing by banking or financial authorities

- Exempt or Unregulated PTCs – Exempt from full licensing if they serve only related trusts and do not solicit public business

For example:

- Cayman Islands: Offers a regulated and registered PTC regime under the Banks and Trust Companies Act.

- BVI: Allows exempt PTCs under the Financial Services (Exemptions) Regulations.

- Singapore: Provides licensing exemptions under the Trust Companies Act for family PTCs.

- United States (e.g., South Dakota, Delaware): Requires state chartering if operating as a regulated trust company.

- Hong Kong: Does not provide a standalone PTC regime; a private trust company may need a Trust or Company Service Provider (TCSP) licence if it is considered to be carrying on a trust business, while family-only structures must still comply with AML/CFT obligations under AMLO.

Comparison of PTC Regulatory Regimes

|

Jurisdiction

|

Licensing Required

|

AML Obligations

|

Public Business Allowed

|

|---|---|---|---|

|

Cayman Islands

|

Registration required

|

Yes

|

Yes

|

|

BVI

|

Exempt regime

|

Yes

|

Yes

|

|

Singapore

|

Licensing exemption

|

Yes

|

Yes

|

|

United States

|

State charter

|

Yes

|

Yes

|

|

Hong Kong

|

TCSP license may apply

|

Yes

|

Yes

|

What Is a Hong Kong Private Trust Company?

A Hong Kong Private Trust Company is a company incorporated under the Companies Ordinance (Cap. 622) that acts as trustee exclusively for related family trusts, rather than offering trust services to the public.

Unlike offshore jurisdictions with specific PTC statutes, Hong Kong regulates trust activities through general legislation. The relevant legal framework includes:

- Trustee Ordinance (Cap. 29) – Governs trustee powers and duties

- Companies Ordinance (Cap. 622) – Corporate governance and director obligations

- Anti-Money Laundering and Counter-Terrorist Financing Ordinance (AMLO)

- Trust or Company Service Provider (TCSP) Licensing Regime

There is no specific “Private Trust Company Act” in Hong Kong. Instead, regulatory classification depends on whether the company is deemed to be carrying on a “trust business.”

Why Mainland China & Hong Kong UHNW Families Use a PTC

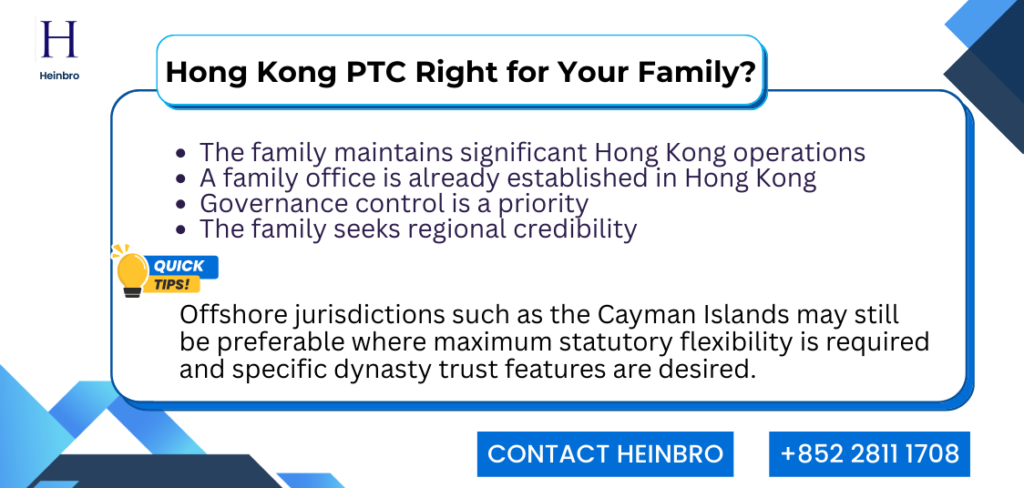

For Mainland China and Hong Kong ultra-high-net-worth (UHNW) families, establishing a Private Trust Company (PTC) in Hong Kong is rarely a purely technical decision. It is typically driven by cross-border realities, generational transition planning, regulatory familiarity, and practical governance needs.

1. Cross-Border Wealth Structuring Between PRC and Hong Kong

Mainland founders frequently hold:

- Offshore holding companies (Cayman or BVI structures)

- Overseas IPO vehicles (U.S. or Hong Kong listings)

- International real estate portfolios (UK, U.S., Singapore, Australia)

- Global investment accounts with private banks

In many cases, the founder resides in Mainland China, key operating companies are in the PRC, the listing vehicle is offshore, and family members are globally mobile. A Hong Kong PTC can serve as a central trustee platform that sits between offshore holding structures and family beneficiaries, offering:

- Enhanced governance credibility in an internationally recognized financial center

- Geographic and legal proximity to Asia-based assets

- Access to Hong Kong’s mature legal, banking, and professional ecosystem

- A bridge between PRC wealth and international markets

Unlike purely offshore jurisdictions, Hong Kong offers a combination of international legal standards and cultural familiarity for Chinese families.

2. Real Scenario: Children Studying Overseas, Assets in Asia

A common real-life situation among Mainland and Hong Kong UHNW families is this:

- The founder remains based in China or Hong Kong

- Core business assets are located in Mainland China or Asia

- Children are educated in the United States, United Kingdom, Canada, or Australia

- Some family members may eventually obtain foreign residency

This creates structural complexity:

- Different tax residencies

- Different legal systems

- Different inheritance regimes

In this context, Hong Kong often becomes the most flexible, familiar, and practical trustee location because:

- It operates under common law, which is widely recognized internationally

- It maintains strong connectivity with Mainland China

- It offers political and financial stability

- It avoids the perception risk sometimes associated with small offshore jurisdictions

A Hong Kong private trust company allows the family to centralize governance in a jurisdiction that is:

- Close to the family’s core wealth

- Understandable to the founder generation

- Recognized by international advisors

This balance is particularly attractive when the next generation resides abroad but the wealth base remains in Asia.

3. Integration with Hong Kong Family Office Structures

Many Mainland families establish a Single-Family Office (SFO) in Hong Kong. A PTC can operate alongside the family office to:

- Formalize trustee decision-making

- Separate asset management from fiduciary duties

- Provide institutional structure while retaining family influence

This separation is legally important. The family office may manage investments, while the PTC acts strictly as trustee—reducing regulatory risk and clarifying responsibilities.

The PTC board may include family representatives, independent directors and legal and compliance advisors. This hybrid governance model balances control and fiduciary responsibility. For entrepreneurial families, this structure provides institutional strength without surrendering authority to an external corporate trustee.

4. Succession Planning for First-Generation Founders

Many first-generation Chinese entrepreneurs face similar concerns:

- How to retain strategic influence while alive

- How to prevent family disputes after succession

- How to ensure business continuity

- How to avoid forced asset fragmentation

A Hong Kong private trust company allows founders to participate at the board level while maintaining proper fiduciary separation between ownership and beneficial interests. This is particularly important where:

- Multiple children are involved

- Some heirs are active in the business, others are not

- Spouses from different jurisdictions are involved

- Assets span multiple legal systems

A PTC can create a structured governance environment that reduces emotional decision-making during times of crisis.

Hong Kong Private Trust Company Regulation

Regulatory analysis is the most critical component of a Hong Kong PTC structure.Under Hong Kong law, any person or entity carrying on a trust or company service business must obtain a Trust or Company Service Provider (TCSP) licence, unless an exemption applies.

When Is a TCSP Licence Required?

A licence is generally required if the company:

- Provides trust services to the public

- Holds itself out as offering trustee services

- Conducts trust administration as a business

For Exceptions, a Hong Kong PTC should :

- Acts solely as trustee for related family trusts

- Does not solicit public business

- Does not provide trustee services for remuneration to third parties

It may fall outside full licensing requirements. However, this analysis must be conducted carefully to avoid regulatory breaches.

AML & AMLO Compliance Requirements

Even if exempt from TCSP licensing, AML obligations under AMLO still apply.

Key requirements include:

- Customer Due Diligence (CDD) on settlors and beneficiaries

- Identification of Ultimate Beneficial Owners (UBO)

- Maintenance of Significant Controllers Register

- Suspicious Transaction Reporting

Hong Kong aligns closely with FATF standards, meaning scrutiny of family structures has increased.

Securities and Futures Commission (SFC) License

If the PTC engages in activities beyond purely acting as trustee, SFC licensing requirements may be triggered, including where it:

- Managing investment portfolios directly

- Providing asset management services

- Exercising discretionary investment authority

Where a family office structure overlaps with trustee functions, Type 9 (asset management) licensing may become relevant unless exemptions apply.

A properly structured model should:

- Separate trustee decision-making from regulated asset management

- Document governance policies clearly

- Obtain formal legal opinions where necessary

Inland Revenue Considerations

Hong Kong applies a territorial tax system, meaning only profits sourced in Hong Kong are taxable.

Key issues include:

- Whether trustee fees are taxable

- Whether underlying trust income is Hong Kong-sourced

- Stamp duty implications

- Risk of PRC tax residency classification

Cross-border tax planning between PRC and Hong Kong must be coordinated carefully.

Structuring a Hong Kong Private Trust Company for China Families

To avoid estate exposure, shares of the PTC are often held by:

- A purpose trust (offshore)

- A foundation

- A nominee under structured governance

Direct founder ownership is generally discouraged for succession planning reasons.

Board Composition Best Practices

For Mainland China families, best practice includes:

- At least one independent professional director

- Clear conflict-of-interest policy

- Formal board minutes

- Distribution committee framework

Strong governance documentation protects both family members and directors.

Interaction with PRC Law

While the PTC is incorporated in Hong Kong, Mainland considerations include:

- Foreign exchange controls

- SAFE reporting obligations

- PRC tax residency of individuals

- Controlled Foreign Corporation (CFC) implications

A Hong Kong PTC does not eliminate PRC regulatory exposure. Cross-border compliance remains critical.

Is a Hong Kong Private Trust Company Right for Your Family?

Building a Compliant Hong Kong Private Trust Company

For Hong Kong and Mainland China UHNW families, a Private Trust Company can serve as a powerful governance platform bridging PRC entrepreneurial wealth and international asset structures. However, regulatory classification under the TCSP regime, AML compliance under AMLO, and potential SFC licensing risks require careful legal analysis.

A poorly structured PTC can expose families to regulatory penalties and cross-border tax risk. A properly structured one enhances governance continuity and regulatory credibility.

Heinbro combines deep regulatory expertise with hands-on operational support for financial services firms. Heinbro provides one-stop compliance services for Hong Kong financial firms, including:

- TCSP licensing applications

- SFC regulatory advisory

- Establishment and immigration support

- Ongoing compliance and inspection preparation

- Recruitment and operational resourcing

For Mainland China and Hong Kong families establishing a private trust company, partnering with experienced compliance professionals ensures regulatory clarity, operational stability, and sustainable multi-generational governance. If you would like to arrange a free consultation, please email heinbro@heinbro.com or call +852 2811 1708.