How to Set Up a Holding Company in Hong Kong: Complete Legal Guide 2026

Hong Kong remains a leading jurisdiction for holding companies, offering tax efficiency, strategic access to Asia, and a business-friendly legal system. It enables multinational groups to centralize ownership and streamline cross-border operations. However, in 2026, regulatory scrutiny and compliance expectations are higher than ever. What are the exact legal steps, and how can businesses mitigate compliance risks? This guide provides a step-by-step legal and compliance roadmap to establishing a Hong Kong holding company effectively.

What Is a Holding Company in Hong Kong?

A holding company in Hong Kong is a legal entity established primarily to own shares in other companies, rather than to conduct operational business activities directly. It functions as a control and asset management vehicle, overseeing subsidiaries across different jurisdictions.

There are two primary types:

- Pure Holding Company: A structure solely used for holding investments and shares, with no operational activities.

- Mixed Activity Holding Company: A hybrid structure that combines holding functions with limited operational activities such as management services or treasury functions.

From a legal standpoint, the distinction is important as it affects tax treatment, substance requirements, and compliance obligations.

Common Use Cases of Hong Kong Holding Companies

Hong Kong holding structures are widely used in the following scenarios:

- Regional Investment Platform: Centralizing investments across Asia under one jurisdiction

- Intellectual Property (IP) Holding: Managing and licensing IP assets efficiently

- Group Restructuring: Streamlining ownership structures for M&A or IPO readiness

- Offshore Tax Planning (Legally Structured): Leveraging Hong Kong’s territorial tax regime within regulatory boundaries

Why Investors Use a Hong Kong Holding Company

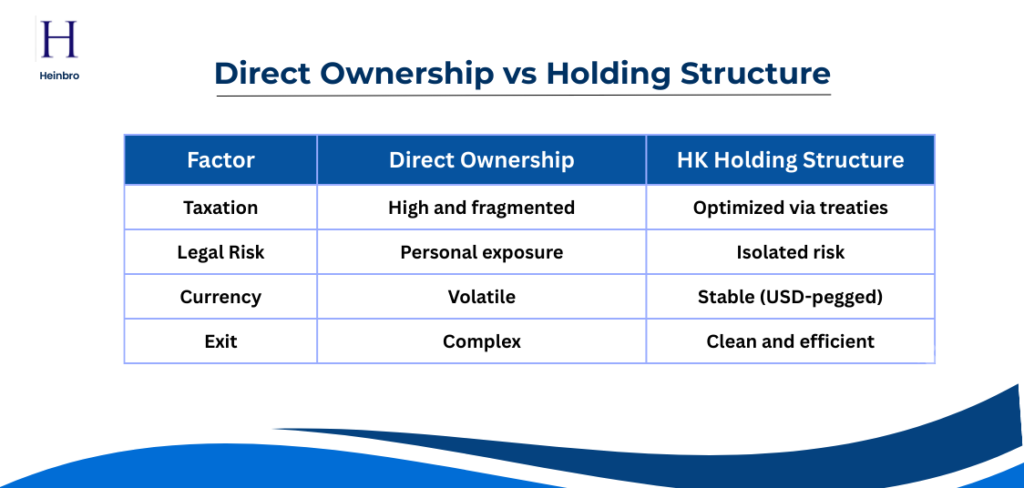

The Problem: Fragmented Regional Ownership Creates Legal and Tax Inefficiencies

Direct ownership of assets across jurisdictions such as Vietnam, Japan, Indonesia, and Thailand exposes businesses to:

- Multiple layers of withholding taxes

- Currency volatility risks

- Overlapping regulatory regimes

- Direct legal liability at the shareholder level

From a legal structuring perspective, this fragmentation increases both compliance burden and litigation exposure, particularly in emerging markets with evolving regulatory frameworks.

The Solution: Centralizing Ownership Through a Hong Kong Holding Company

A Hong Kong holding company functions as a centralized legal and financial control hub. Instead of owning assets directly, investors hold regional subsidiaries through a single Hong Kong entity.

This structure enables:

- Consolidated ownership and governance

- Streamlined reporting and compliance

- Reduced exposure to local jurisdictional risks

- Enhanced capital allocation efficiency

From a corporate law standpoint, this model introduces jurisdictional clarity and operational scalability.

The Advanced Ownership Structure: Layered Protection and Control

Sophisticated investors rarely rely on a single-layer structure. A typical institutional-grade setup includes:

- Family Trust – ultimate beneficial ownership and succession planning

- Offshore Entity (BVI/Cayman) – privacy and asset protection layer

- Hong Kong Holding Company – operational and financial hub

- Local Subsidiaries – country-specific operations

This layered architecture ensures legal separation between control, ownership, and operational risk, which is critical for cross-border asset protection.

Key Benefits of Setting Up a Holding Company in Hong Kong

Tax Advantages of Hong Kong Holding Company

Hong Kong applies a territorial basis of taxation, meaning only profits sourced within Hong Kong are subject to tax.

- Offshore income may be exempt, subject to foreign-sourced income exemption (FSIE) rules, economic substance, and proper documentation

- No capital gains tax on disposal of investments, enhancing exit efficiency

- No withholding tax on dividends, allowing tax-efficient profit repatriation to shareholders

These features make Hong Kong particularly attractive for cross-border structuring and investment holding.

Double Tax Treaties and China Market Access

Hong Kong maintains an extensive network of 56 Comprehensive Double Taxation Agreements (CDTAs) as of March 2026, enabling:

- Reduced withholding tax rates on cross-border payments

- Efficient dividend repatriation

- Greater tax certainty in international structuring

Under the Mainland China–Hong Kong arrangement:

- Dividend withholding tax may be reduced from 10% to 5% where the Hong Kong entity is the beneficial owner and holds at least 25% of the Mainland company (subject to treaty and anti-abuse rules)

This continues to position Hong Kong as a strategic gateway for Mainland China investment, offering tax efficiency alongside a familiar legal and financial environment.

Flexibility in Corporate Structure

Hong Kong offers significant structural flexibility:

- 100% foreign ownership permitted

- No minimum share capital requirement

- Simple and fast incorporation process

This enables businesses to design tailored holding structures aligned with commercial objectives.

Legal Protection Under Common Law System

Hong Kong’s legal framework is based on common law, providing:

- Strong protection of shareholder rights

- Predictable judicial outcomes

- Clear corporate governance standards

A properly structured holding company isolates liabilities, ensuring that risks at the subsidiary level do not automatically extend to the parent entity.

Currency Stability and Institutional Banking Access

Hong Kong offers a highly developed financial ecosystem:

- HKD is pegged to USD, reducing FX volatility

- Access to global Tier-1 banks (e.g., HSBC, Citi, Standard Chartered)

- Multi-currency treasury management capabilities

This is particularly valuable for businesses operating across multiple Asian currencies.

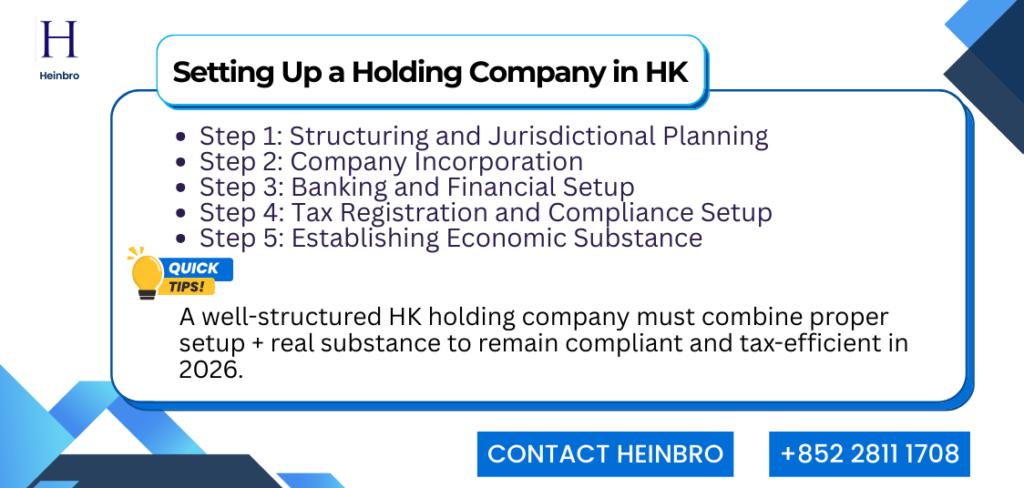

Step-by-Step Guide to Setting Up a Holding Company in Hong Kong

Step 1: Structuring and Jurisdictional Planning

Before incorporation, businesses must determine:

- Ownership layers (trust, offshore, HK entity)

- Jurisdiction of subsidiaries

- Tax and legal implications across jurisdictions

This step is critical, as improper structuring can lead to loss of tax benefits or regulatory challenges.

Step 2: Company Incorporation

Key requirements include:

- At least one director (individual)

- At least one shareholder

- A company secretary (mandatory)

- A registered Hong Kong address

Incorporation is completed through the Companies Registry, typically within 1–3 business days.

Step 3: Banking and Financial Setup

Opening a corporate bank account requires:

- Detailed KYC documentation

- Business plan and operational rationale

- Source-of-funds verification

- Economic substance requirements

Step 4: Tax Registration and Compliance Setup

Companies must obtain a Business Registration Certificate and comply with:

- Inland Revenue Department (IRD) requirements

- Ongoing accounting and audit obligations

- Annual return filings

Step 5: Establishing Economic Substance

Increased global tax transparency has led to stricter enforcement:

- Offshore tax claims require demonstrable economic substance

- Tax authorities may challenge artificial structures

- Real decision-making and control must be evidenced

Failure to meet these requirements can result in tax reassessments and penalties.

Taxation Advantages of Holding Companies in Hong Kong

Profits Tax and Offshore Claims

- Tax rates: 8.25% (first HKD 2M) and 16.5% thereafter

- Offshore income may be exempt if properly structured

However, offshore status must be supported by robust documentation and operational evidence.

Dividend and Capital Gains Treatment

Hong Kong’s tax regime allows:

- Tax-free dividend inflows

- Efficient redistribution to shareholders

This enhances investment efficiency and exit flexibility.

Treasury and Currency Management

A Hong Kong holding company can act as a regional treasury center, enabling:

- Currency consolidation into USD/HKD

- Reduced FX risk exposure

- Centralized liquidity management

Double Taxation Agreements (DTAs)

Hong Kong’s extensive DTA network provides:

- Reduced withholding taxes

- Improved cross-border tax efficiency

- Greater certainty in international structuring

Exit Strategy for Hong Kong Holding Companies

Challenges of Direct Asset Disposal

Selling assets individually across jurisdictions typically involves:

- Multiple capital gains tax liabilities

- Complex regulatory approvals

- Extended transaction timelines

The Clean Exit Model

Instead of selling underlying assets, investors sell shares of the Hong Kong holding company.

Key advantages:

- Single transaction under Hong Kong law

- No capital gains tax in Hong Kong

- Faster execution and liquidity

This approach is widely adopted in private equity and cross-border M&A structures.

Interaction with PRC Law

While the PTC is incorporated in Hong Kong, Mainland considerations include:

- Foreign exchange controls

- SAFE reporting obligations

- PRC tax residency of individuals

- Controlled Foreign Corporation (CFC) implications

A Hong Kong PTC does not eliminate PRC regulatory exposure. Cross-border compliance remains critical.

Key 2026 Updates for Hong Kong Holding Companies

Global Minimum Tax (Pillar Two) Considerations

For large multinational groups, Global Minimum Tax and Hong Kong Minimum Top-up Tax now apply:

- A 15% global minimum effective tax rate is introduced

- Hong Kong has implemented the Hong Kong Minimum Top-up Tax (HKMTT)

- Applies to fiscal years beginning on or after 1 January 2025

Impact:

- Purely tax-driven holding structures are less effective

- Groups must assess global effective tax rates

- Greater emphasis on economic substance and compliant structuring

Stronger Economic Substance Requirements (FSIE Regime)

The expanded Foreign-Sourced Income Exemption (FSIE) regime introduces stricter conditions:

- Increased documentation requirements

- Requirement to demonstrate real business activities in Hong Kong

Impact:

- Shell or passive holding companies face heightened scrutiny

- Companies must demonstrate:

- Local management and control

- Presence of employees and/or office

- Substantive decision-making in Hong Kong

Is Hong Kong Still the Optimal Holding Jurisdiction in 2026?

Advantages

- Tax efficiency under territorial system

- Strong legal infrastructure

- Strategic gateway to Asia and China

Considerations

- Increasing regulatory scrutiny

- Higher compliance expectations

- Banking due diligence requirements

Hong Kong remains a leading holding company jurisdiction, but the framework has shifted toward a substance-based, compliance-driven model, requiring more robust structuring, governance, and documentation in 2026 and beyond.

Building a Compliant and Scalable Holding Structure

Setting up a holding company in Hong Kong requires more than simple incorporation—it demands careful legal structuring, tax planning, and ongoing compliance management. When executed correctly, it offers a powerful framework for managing regional investments, protecting assets, and optimizing exits.

In this increasingly regulated environment, working with a professional partner is critical. Heinbro provides a comprehensive, one-stop compliance solution for Hong Kong financial and corporate structures. From company formation and licensing to ongoing compliance, inspection support, training, and recruitment, Heinbro combines deep regulatory expertise with practical operational support—helping businesses build resilient, compliant, and scalable holding structures across Asia. For a free initial consultation, please contact Heinbro at heinbro@heinbro.com or by phone at +852 2811 1708.