Hong Kong ESG Reporting 2025 Update: New Climate Mandates

Are Hong Kong companies fully prepared for the tightening ESG reporting regime?

With HKEX strengthening sustainability disclosure requirements and climate reporting aligning with IFRS S2 and international standards, ESG reporting is no longer a voluntary branding exercise—it is a regulatory obligation. Non-compliance may expose listed companies and financial institutions to enforcement action, reputational damage, and investor scrutiny. This guide explains Hong Kong ESG reporting requirements, climate disclosure obligations, and a practical compliance roadmap.

This article is designed as a high-authority, production-ready ESG compliance reference for boards, compliance officers, in-house counsel, and financial services professionals.

Evolution of HKEX ESG Reporting Requirements

Hong Kong ESG reporting has evolved significantly over the past decade. Initially introduced as a voluntary framework, the HKEX ESG Reporting Guide has gradually transitioned into a mandatory disclosure regime under the Listing Rules.

Key Milestones in Regulatory Development

- Introduction of the ESG Reporting Guide under Appendix 27

- Transition to Appendix C2 (ESG Code)

- Shift from voluntary reporting to “comply or explain”

- Mandatory disclosure of key environmental KPIs

- Formal board responsibility for ESG governance

- Alignment with TCFD recommendations

- Movement toward IFRS Sustainability Disclosure Standards (IFRS S1 and IFRS S2)

Today, ESG disclosure is embedded within Hong Kong’s listing compliance framework under Main Board Rule 13.91 & Appendix C2 and GEM Rule 17.103 & Appendix C2. Boards are expressly responsible for oversight of ESG risks and strategy.

Who Must Comply with Hong Kong ESG Reporting Rules?

The following entities are primarily affected:

- Main Board listed companies

- GEM listed companies

- Financial institutions regulated by the SFC

- Asset managers subject to climate-related risk management requirements

In practice, even private companies and subsidiaries are indirectly affected due to supply chain transparency, investor due diligence requirements, and cross-border regulatory alignment.

Important Requirements for HKEX ESG Reporting

Mandatory Disclosure Obligations under HKEX

Under the ESG Reporting Code (Appendix C2), listed issuers are required to make structured disclosures across governance, risk management, reporting principles, environmental metrics, and social KPIs. These obligations form part of the Listing Rules and are subject to regulatory oversight.

- Governance Structure

- Board oversight of ESG matters

- Management’s role in ESG implementation

- Risk Management

- Identification and assessment of ESG risks

- Integration into enterprise risk management systems

- Reporting Principles

- Materiality

- Quantitative disclosure

- Consistency and comparability

Failure to properly explain omissions under the “comply or explain” principle may attract regulatory attention.

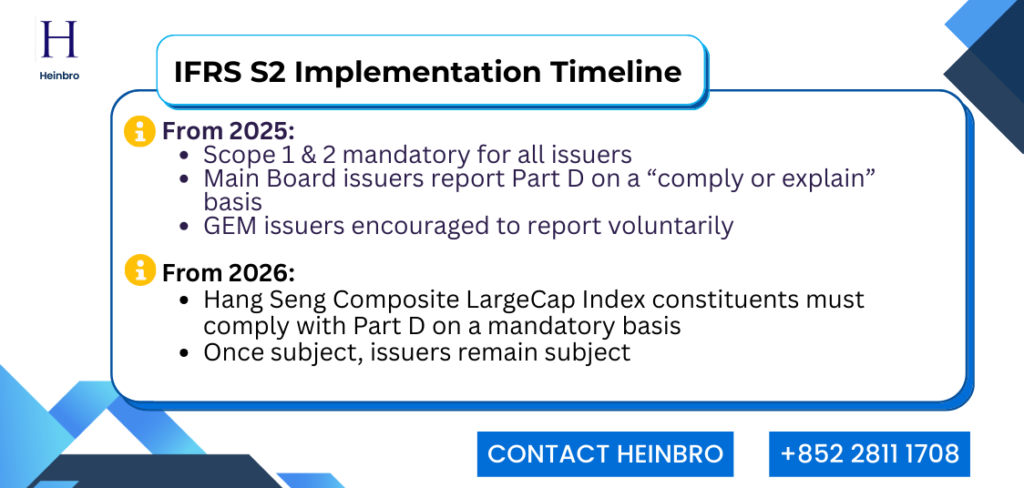

IFRS S2 Implementation Timeline in Hong Kong

Hong Kong has signaled its intention to align with ISSB standards. Large listed companies are expected to implement enhanced climate disclosures progressively from 2025 onward.

Early preparation is strongly recommended.

Environmental Disclosure Obligations

Environmental disclosures under HKEX require clear, quantitative reporting of climate-related metrics. Issuers must disclose:

- Scope 1 greenhouse gas emissions (direct emissions)

- Scope 2 greenhouse gas emissions (indirect emissions from purchased energy)

- Scope 3 greenhouse gas emissions, including mapping against the 15 GHG Protocol categories and justification for any exclusions

- Energy consumption intensity

- Water usage and efficiency

- Waste generation and recycling data

- Climate-related targets and mitigation measures

Scope 3 Emissions – Value Chain Mapping Requirement

Scope 3 reporting encompasses emissions across upstream and downstream value chains, including purchased goods, transportation, use of sold products, and investments.

This significantly increases reporting complexity, particularly for:

- Multinational issuers

- Manufacturing groups

- Financial institutions (where financed emissions fall under Scope 3 Category 15)

While not all Scope 3 categories must necessarily be quantified at inception, issuers must demonstrate a structured and defensible mapping exercise.

Implementation Relief Mechanisms (Climate-Related)

Where applicable, issuers may rely on limited relief provisions, including:

- Reasonable information relief (use available data without undue cost or effort)

- Capabilities relief (aligned with internal resources)

- Commercial sensitivity relief (limited exemption for sensitive climate opportunity data)

- Financial effects relief (qualitative disclosure where quantitative data is unavailable)

Social Disclosure Obligations

Social KPIs remain mandatory under Part C of Appendix C2 and include:

- Employment and labor standards

- Health and workplace safety statistics

- Supply chain ESG risk management

- Anti-corruption policies, training, and enforcement

- Community investment and engagement

These disclosures must be supported by measurable KPIs rather than generic statements. Generic policy statements without quantitative backing or operational evidence may be regarded as insufficient.

Climate Disclosure Requirements in Hong Kong

Alignment with TCFD and IFRS S2 Standards

Hong Kong regulators have aligned climate reporting with the Task Force on Climate-related Financial Disclosures (TCFD) framework and are transitioning toward IFRS S2 Climate-related Disclosures.

Climate reporting requires disclosure under four pillars:

- Governance – Board oversight of climate risks

- Strategy – Climate-related impacts on business model and financial planning

- Risk Management – Processes for identifying and managing climate risks

- Metrics and Targets – Emissions data and decarbonization goals

This moves ESG reporting from qualitative narrative to financially material climate risk analysis.

How ESG Reporting Impacts Financial Services Firms in Hong Kong

Financed emissions fall under Scope 3 Category 15 (investments). Asset managers, commercial banks, and insurers must:

- Include financed emissions in Scope 3 reporting

- Justify exclusions

- Consider alignment with IFRS S2 Application Guidance

For licensed corporations and asset managers, ESG reporting intersects directly with regulatory compliance obligations.

Step-by-Step Compliance Strategy for Hong Kong ESG Reporting

Step 1 – Conduct a Gap Analysis

Compare current disclosures against:

- HKEX ESG Reporting Code

- TCFD recommendations

- IFRS S2 requirements

- GHG Protocol Scope 1–3

Identify missing data points, particularly in:

- Mandatory Scope 1 and Scope 2 emissions

- Scope 3 value chain mapping

- Climate-related financial impact disclosures

- Governance documentation

This step establishes the regulatory baseline for 2025–2026 compliance.

Step 2 – Establish Robust ESG Governance

Best practice includes:

- Assigning board-level accountability

- Forming an ESG or sustainability committee

- Documenting oversight processes

- Integrating ESG into corporate strategy

In addition, issuers should:

- Assess whether they are a Hang Seng Composite LargeCap Index (HSCLI) constituent

- Determine their mandatory climate disclosure exposure timeline

Regulators increasingly expect demonstrable board involvement and forward-looking regulatory planning.

Step 3 – Implement Data Collection and Internal Controls

Accurate ESG reporting requires:

- Carbon accounting systems

- Centralized ESG data platforms

- Internal audit review

- Cross-department coordination

At this stage, issuers should also:

- Assess whether implementation relief mechanisms apply (e.g., reasonable information, capabilities, commercial sensitivity, financial effects relief)

- Document clear justification where relying on any relief provisions

Poor data quality and undocumented reliance on relief provisions are common compliance weaknesses.

Step 4 – Draft, Review, and Assure the ESG Report

Before publication:

- Conduct legal and compliance review

- Ensure consistency with annual financial statements

- Confirm reporting boundary transparency

- Validate climate-related financial disclosures

Consider obtaining ISSA 5000–aligned third-party assurance (the global sustainability assurance baseline published in November 2024) to enhance ESG credibility. Independent assurance strengthens investor confidence and mitigates greenwashing risk.

Common ESG Reporting Compliance Risks in Hong Kong

Greenwashing and Misleading Disclosure

The Securities and Futures Commission (SFC) has increased scrutiny on misleading ESG claims. Overstating sustainability achievements or omitting material climate risks may lead to:

- Regulatory investigation

- Public reprimand

- Investor litigation

- Reputational harm

ESG disclosures must be substantiated by verifiable data.

Inadequate Climate Risk Assessment

A common failure involves treating climate risks as peripheral rather than financially material. If climate-related risks contradict financial statement assumptions, regulators may question governance integrity.

Strengthening ESG Compliance in Hong Kong

Hong Kong ESG reporting is rapidly evolving toward global sustainability standards. With HKEX requirements tightening and IFRS S2 climate disclosure on the horizon, companies must treat ESG compliance as a core governance function rather than a marketing initiative.

Proactive compliance—through governance enhancement, accurate data systems, and legal review—significantly reduces regulatory and reputational risk.

Heinbro provides comprehensive compliance support for financial firms in Hong Kong, combining regulatory expertise with practical execution. By embedding ESG within broader regulatory frameworks, Heinbro helps firms build robust, sustainable governance in an increasingly complex environment. Contact Heinbro at heinbro@heinbro.com or call +852 2811 1708 to book a free consultation.