How to Set Up a Family Office in Hong Kong: Structure & Tax

Hong Kong has firmly established itself as a premier jurisdiction for the formation of single-family offices (SFOs), driven by a combination of tax efficiency, regulatory clarity, and strategic access to Asian markets. Recent legislative developments—most notably the Inland Revenue (Amendment) (Tax Concessions for Family-owned Investment Holding Vehicles) Ordinance 2023—have significantly enhanced its attractiveness for ultra-high-net-worth families.

However, these advantages depend on proper structuring and compliance. Establishing a family office in Hong Kong requires careful alignment of tax eligibility, licensing considerations, and operational substance. This guide provides a comprehensive, practitioner-level overview of how to set up a family office in Hong Kong.

What Is a Family Office in Hong Kong?

Single Family Office vs Multi-Family Office

A Single Family Office (SFO) is established to manage the assets of a single family and is typically structured as a private company. From a regulatory perspective, SFOs benefit from greater flexibility, particularly where activities are conducted on a non-commercial or cost-recovery basis.

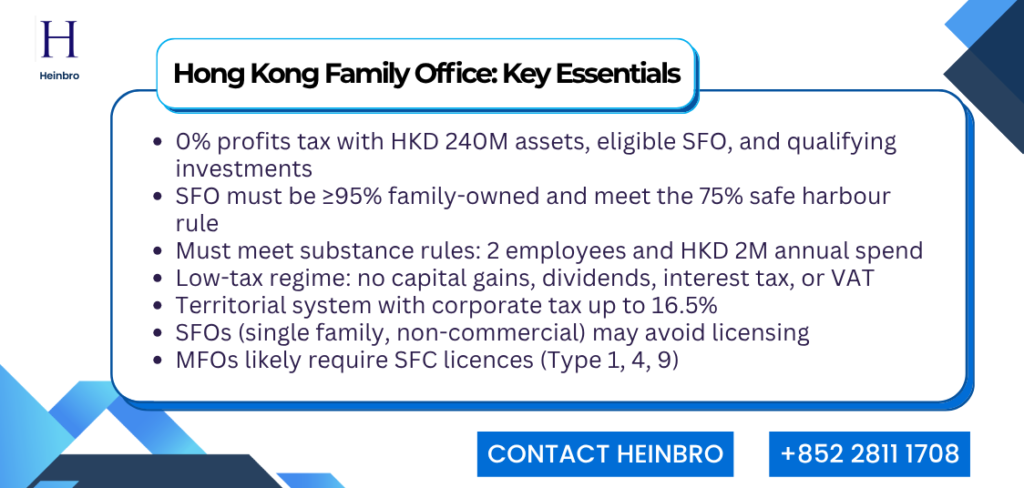

By contrast, a Multi-Family Office (MFO) serves multiple unrelated families and is generally regarded as a commercial enterprise. As such, it is more likely to trigger licensing requirements under the Securities and Futures Ordinance (SFO), including:

- Type 1 (Dealing in Securities)

- Type 4 (Advising on Securities)

- Type 9 (Asset Management)

Typical Family Office Structure in Hong Kong

A standard Hong Kong family office structure includes:

- Family-owned Investment Holding Vehicle (FIHV): Holds and manages investment assets

- Single Family Office (SFO): Provides investment management services to the FIHV

- Trust or Holding Entity: Enhances succession planning and asset protection

Ownership structures often involve a common holding company or trust arrangement, where the SFO manages assets on behalf of the family or a trustee.

Why Set Up a Family Office in Hong Kong?

0% Profits Tax Under FIHV Regime

Under the Inland Revenue (Amendment) Ordinance 2023, qualifying Family-owned Investment Holding Vehicles (FIHVs) managed by eligible single-family offices may benefit from a profits tax exemption on qualifying transactions and incidental transactions, provided that specific conditions are met, including minimum asset thresholds and substantial economic substance requirements.

No Capital Gains Tax & Investment Flexibility

Hong Kong does not impose capital gains tax, dividend withholding tax, or tax on interest income. Combined with its territorial tax system—where only Hong Kong-sourced income is taxable—this allows family offices to deploy capital globally with minimal tax leakage and high structural flexibility.

Capital Investment Entrant Scheme (CIES): Residency Strategy

The Capital Investment Entrant Scheme (relaunched 2024) provides a complementary pathway:

- Minimum HKD 30 million investment

- HKD 3 million allocated to government portfolio

- Permanent residency eligibility after 7 years

This enables families to align wealth structuring with physical relocation strategy.

Key Considerations for Setting Up a Family Office in Hong Kong

The Profits Tax Concession Regime

The cornerstone of Hong Kong’s family office regime is the profits tax concession introduced in 2023. To qualify for a 0% profits tax rate, the FIHV must:

- Be managed or controlled in Hong Kong

- Be managed by an eligible SFO

- Maintain a minimum asset threshold of HKD 240 million

- Invest in specified asset classes, including securities, bonds, funds, and private companies

- Not operate as a general commercial or industrial business

Additionally, the regime extends to Family-owned Special Purpose Entities (FSPEs) linked to the FIHV.

Eligible Single Family Office Requirements

An SFO must:

- Be a private company controlled by a single family (≥95% ownership)

- Satisfy the “safe harbour rule”: At least 75% of assessable profits must derive from services provided to the family

Failure to meet this threshold may result in loss of tax concession eligibility.

Substantial Activities Requirement

To ensure economic substance, Hong Kong requires:

- At least 2 full-time employees in Hong Kong

- Minimum HKD 2 million annual operating expenditure

This requirement is strictly enforced and forms a key audit focus.

Hong Kong’s Broader Tax Environment

The FIHV regime operates within one of the most competitive tax systems globally:

- No capital gains tax

- No dividend or interest tax

- No VAT or sales tax

- Territorial taxation principle (only Hong Kong-sourced income taxed)

- Corporate tax capped at 16.5% (or 8.25% for first HKD 2M)

In addition, Hong Kong maintains an extensive double taxation treaty network, enhancing cross-border structuring certainty.

Licensing Requirements

Under the SFO, licensing is required if all three conditions are met:

- The activity constitutes a regulated activity

- The activity is conducted as a business

- The activity is carried out in Hong Kong

An SFO may not require a licence if:

- It operates on a cost-recovery basis

- It does not pursue profit as a business objective

- Services are provided solely to group entities or the family

To mitigate licensing risk, practitioners typically adopt:

- Group company exemption structures

- Outsourcing regulated activities to licensed asset managers

- Structuring investment decisions at the FIHV or board level

Step-by-Step: Setting Up a Family Office in Hong Kong

Step 1 – Define Family Objectives & Governance

Clarify whether the focus is:

- Wealth preservation vs growth

- Intergenerational transfer

- Geographic investment focus

Establish governance frameworks, including family charters and decision-making protocols.

Step 2 – Choose the Legal Structure

Select appropriate vehicles:

- FIHV (company, LPF, or trust-owned entity)

- SFO management company

- Optional trust layer for succession

Each has implications for tax, control, and inheritance.

Step 3 – Incorporate Entities

Register The investment holding entity (FIHV) or The management company (SFO) with the Companies Registry and ensure:

- Central management and control in Hong Kong

- Proper shareholder and governance documentation

Step 4 – Open Bank Accounts & Allocate Assets

Engage private banks (e.g., HSBC, UBS) and transfer assets into the FIHV. Robust KYC/AML checks will apply.

Step 5 – Apply for Tax Concessions

Submit for advance rulings or ensure compliance with the tax exemption regime under Hong Kong Inland Revenue Department guidelines.

Step 6 – Hire Staff & Establish Operations

Recruit investment professionals, compliance officers, and accountants to meet substance requirements and operational needs. Establish internal controls and reporting systems, and maintain expenditure thresholds.

Ongoing Compliances for Hong Kong Family Offices

AML & KYC Requirements

Family offices must comply with Hong Kong’s strict anti-money laundering regulations, especially when onboarding banking relationships.

Ongoing Reporting & Audit Obligations

- Annual financial statements

- Tax filings

- Possible audits

Compliance failures can jeopardize tax benefits.

Risk Management & Governance Framework

Implement internal controls, investment committees, and clear reporting lines to manage operational and fiduciary risks.

Costs of Setting Up a Family Office in Hong Kong

Initial Setup Costs

- Legal and advisory fees

- Company incorporation

- Structuring and tax planning

Ongoing Operational Costs

- Salaries for qualified staff

- Office rental and administration

- Compliance and audit expenses

Typically, annual operating costs must exceed HKD 2 million to meet substance requirements.

Hong Kong vs Singapore: Which Is Better for Family Office Setup?

Choosing between Hong Kong and Singapore is not a matter of which jurisdiction is “better” overall, but rather which is better aligned with your family’s structure, risk appetite, and strategic objectives. The two regimes are fundamentally different in how they approach tax, regulation, and operational design.

|

Key Factor

|

Hong Kong

|

Singapore

|

|---|---|---|

|

Tax Regime

|

0% profits tax on qualifying transactions under FIHV regime (subject to conditions)

|

Tax exemption under Sections 13O / 13U (pre-approved by MAS)

|

|

Approval Process

|

No formal pre-approval (self-assessment + IRD review)

|

Mandatory pre-approval by MAS before tax benefits apply

|

|

Minimum Assets (AUM)

|

HKD 240 million (~USD 30M)

|

SGD 10M–20M (~USD 7M–15M)

|

|

Regulatory Approach

|

Flexible, principle-based

|

Structured, rules-based

|

|

Market Access

|

Strong China + Greater Bay Area access

|

Strong Southeast Asia + global investment hub

|

|

Setup Complexity

|

Faster setup, less upfront regulatory friction

|

More complex due to approval process

|

Which Jurisdiction Should You Choose?

- Choose Hong Kong if your priority is tax efficiency, flexible structuring, and access to China-related opportunities, and you can meet higher asset and substance thresholds.

- Choose Singapore if you value regulatory certainty, lower entry barriers, and a highly structured compliance environment.

In practice, some ultra-high-net-worth families adopt a dual-jurisdiction strategy, leveraging Hong Kong for China-facing investments and Singapore for broader regional diversification.

From Setup to Compliance for a Family Office in Hong Kong

Setting up a family office in Hong Kong offers significant advantages—from 0% profits tax to unmatched access to China markets. However, achieving these benefits requires careful structuring, strict compliance, and ongoing operational discipline.

This is where Heinbro becomes a strategic partner. Heinbro combines deep regulatory expertise with hands-on operational support for financial services firms. It provides a one-stop compliance solution for Hong Kong family offices, covering everything from establishment (licensing and immigration), to ongoing operations (compliance, inspection support, training), and long-term growth (recruitment and resourcing). With the right partner, your family office can be both compliant and future-ready. Get in touch with Heinbro at heinbro@heinbro.com, or call +852 2811 1708 to book a free consultation.