Hong Kong Private Equity Fund Administration for LPFs and OFCs

Hong Kong is fast emerging as Asia’s private equity powerhouse — but setting up a Limited Partnership Fund (LPF) or Private Open-Ended Fund Company (Private OFC) is only the first step. With increasing Securities and Futures Commission scrutiny and rising investor expectations for transparency and accurate valuation, fund administration has never been more critical.

This guide breaks down Hong Kong private equity fund administration, covering LPF and OFC structures, NAV calculation, compliance requirements, and key outsourcing considerations.

What Is Private Equity Fund Administration in Hong Kong?

Private equity fund administration the operational, accounting, reporting, and compliance processes supporting a fund throughout its lifecycle. In Hong Kong, these services typically include:

- Fund accounting and bookkeeping

- NAV calculation and valuation support

- Capital call and distribution processing

- Financial statement preparation

- Investor reporting

- AML/KYC coordination

- Regulatory compliance support

Regardless of whether the fund is structured, these functions must operate within a robust compliance framework.

Regulatory Context in Hong Kong

In Hong Kong, any entity conducting discretionary asset management business will generally be required to hold a Type 9 (Asset Management) license under the Securities and Futures Ordinance (SFO), unless a specific exemption applies.

It is important to distinguish:

- Fund Manager (Type 9 licensed entity) – Responsible for investment decisions, risk management and regulatory compliance.

- Fund Administrator – Handles operational execution such as fund accounting, NAV calculation, capital call and distribution processing, and reporting.

The SFC expects licensed managers to maintain proper oversight even if fund administration is outsourced.

Hong Kong Common Private Equity Fund Structures

Hong Kong offers two primary onshore fund vehicles:

- Limited Partnership Fund (LPF)

- Private Open-ended Fund Company (Private OFC)

For private equity purposes, OFCs are typically structured as private (non-public) OFCs, meaning their shares are offered only to professional investors and not to the retail public.

Understanding the differences between LPF and OFC is fundamental when structuring a Hong Kong private equity fund. Both structures can house private equity strategies, but their operational mechanics differ significantly.

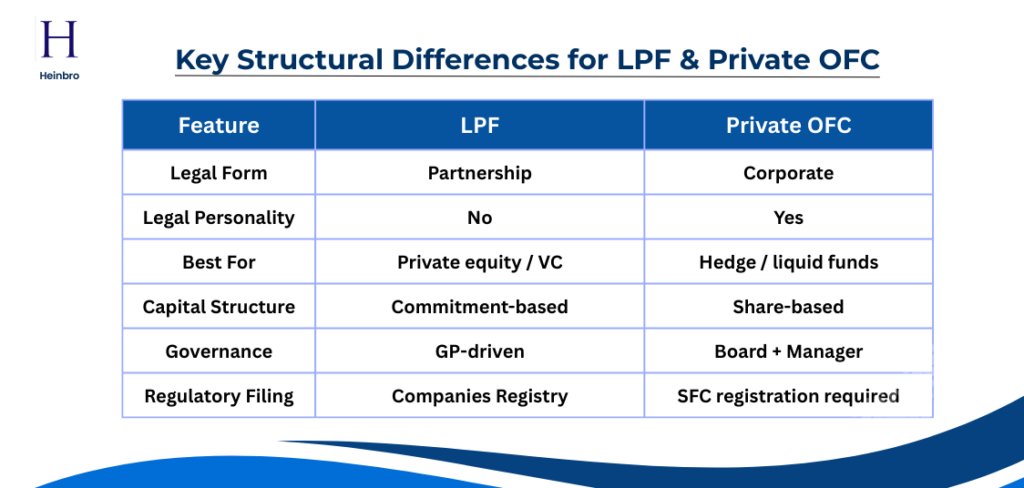

Private OFC vs LPF: Key Structural Differences

Limited Partnership Fund (LPF)

The Limited Partnership Fund (LPF) regime, introduced under the Limited Partnership Fund Ordinance (Cap. 637), is specifically designed for private equity and venture capital funds.

Key Features of LPF:

- Partnership-based structure (no separate legal personality)

- At least one General Partner (GP) and one Limited Partner (LP)

- High contractual flexibility

- Capital commitment model

- Suitable for closed-ended funds

- Profits tax exemption for qualifying transactions

- Carried interest tax concessions (subject to conditions)

Why LPF Is Suitable for Private Equity

Private equity funds typically:

- Draw capital over time

- Invest in illiquid portfolio companies

- Operate on a closed-ended lifecycle

- Distribute profits through waterfall structures

The LPF framework aligns naturally with these operational characteristics.

From a fund administration perspective, LPFs require:

- Capital commitment tracking

- Capital call issuance and drawdown management

- Maintenance of partner registers

- Waterfall distribution calculations

- Register maintenance

- Annual return filing

- Proper custody arrangements

- Audit and valuation governance

Because LPFs operate on a commitment-based model, carried interest and capital account accuracy are central compliance considerations.

Private Open-Ended Fund Company (Private OFC)

The Open-ended Fund Company (OFC) regime, governed under the Securities and Futures Ordinance (Cap. 571), is a corporate fund vehicle with separate legal personality. For private equity purposes, it is typically established as a Private OFC, offered only to professional investors.

Key Features of OFC:

- Corporate structure (separate legal entity)

- Variable share capital

- Suitable for open-ended funds

- Board of directors required

- Must appoint an SFC-licensed investment manager

- Custodian appointment mandatory

When Is a Private OFC Used for PE?

A Private OFC may be considered where:

- A corporate vehicle is preferred

- Investors favor share-based participation

- A hybrid or multi-strategy structure is contemplated

- Tax or cross-border structuring considerations apply

While LPF remains the predominant structure for traditional closed-ended private equity funds, Private OFCs provide a viable corporate alternative.

Capital Contributions, Distributions & Waterfall Structures

The administration of capital flows in a Hong Kong private equity fund depends on whether the vehicle is structured as an LPF (partnership-based) or an OFC (corporate share-based).

For LPF Structures (Commitment-Based Model)

Hong Kong LPFs typically operate on a capital commitment model. Fund administration includes:

- Monitoring capital commitments

- Issuing capital call notices

- Managing drawdowns

- Maintaining partner capital accounts

- Processing distributions

- Calculating carried interest

Two common waterfall models apply:

- European waterfall (whole fund basis)

- American waterfall (deal-by-deal basis)

Accurate documentation and audit-ready calculations are particularly critical where carried interest tax concessions are relied upon.

For Private OFC (Share-Based Model)

Private OFCs operate on a share capital framework rather than partnership capital accounts.

Fund administration typically involves:

- Processing share subscriptions

- Share issuance

- NAV per share calculation

- Distribution declaration (if structured as closed-ended)

- Corporate record maintenance

While economic arrangements may replicate carried interest structures contractually, the accounting treatment differs from traditional LP-style capital accounts.

NAV Calculation for Hong Kong Private Equity Funds

NAV governance applies to both LPF and Private OFC structures where the underlying investment strategy is private equity.

NAV Determination Under HKFRS / IFRS

Unlike hedge funds with daily pricing, private equity NAV is typically calculated quarterly or at defined reporting intervals.

Hong Kong PE funds generally follow:

- HKFRS (Hong Kong Financial Reporting Standards)

- IFRS fair value principles

Valuation methods include:

- Discounted Cash Flow (DCF)

- Comparable company analysis

- Recent transaction benchmarks

Because portfolio companies are illiquid, fair value assessments must be well documented and consistently applied.

SFC Expectations on Valuation Governance

Regardless of vehicle type, the SFC expects Type 9 licensed managers to maintain:

- Independent valuation policies

- Clear documentation of key assumptions

- Conflict-of-interest controls

- Proper segregation of duties

- Robust internal controls

Practical Case Example

A Hong Kong private equity manager delayed impairment recognition for a portfolio company. During an SFC inspection, inadequate valuation documentation triggered regulatory inquiries.

Remediation included:

- Engaging independent valuation advisors

- Updating written valuation policies

- Enhancing internal review procedures

- Strengthening board or GP oversight

This illustrates that NAV governance is directly linked to regulatory risk exposure.

Compliance Requirements for Hong Kong Private Equity Fund

The compliance framework applies at the manager level, regardless of whether the fund is structured as LPF or OFC.

SFC Licensing & Ongoing Obligations

Type 9 licensed managers must comply with:

- Financial Resources Rules (FRR)

- Annual audited accounts submission

- Business conduct requirements

- Risk management and internal control standards

For OFCs, additional SFC registration requirements apply at the fund level. Outsourcing fund administration does not remove regulatory responsibility.

AML / KYC & Investor Due Diligence

Under the Anti-Money Laundering and Counter-Terrorist Financing Ordinance (AMLO), licensed managers must:

- Conduct customer due diligence (CDD)

- Verify beneficial ownership and control structures

- Perform Politically Exposed Person (PEP) screening and apply enhanced due diligence (EDD) where applicable

- Monitor ongoing transactions

- Establish internal reporting and escalation procedures

Additionally, funds must comply with:

- FATCA reporting

- Common Reporting Standard (CRS) obligations

For a detailed overview of AML/CFT requirements applicable to Hong Kong licensed corporations — including internal controls, risk assessments, compliance officer responsibilities, and inspection readiness — refer to Full AML/CFT Compliance Guide.

Record-Keeping and Inspection Risk

Common deficiencies identified in Hong Kong regulatory inspections include:

- Inadequate valuation documentation

- Poor segregation of duties

- Insufficient compliance monitoring

- Weak outsourcing oversight

Robust fund administration systems significantly reduce inspection risk.

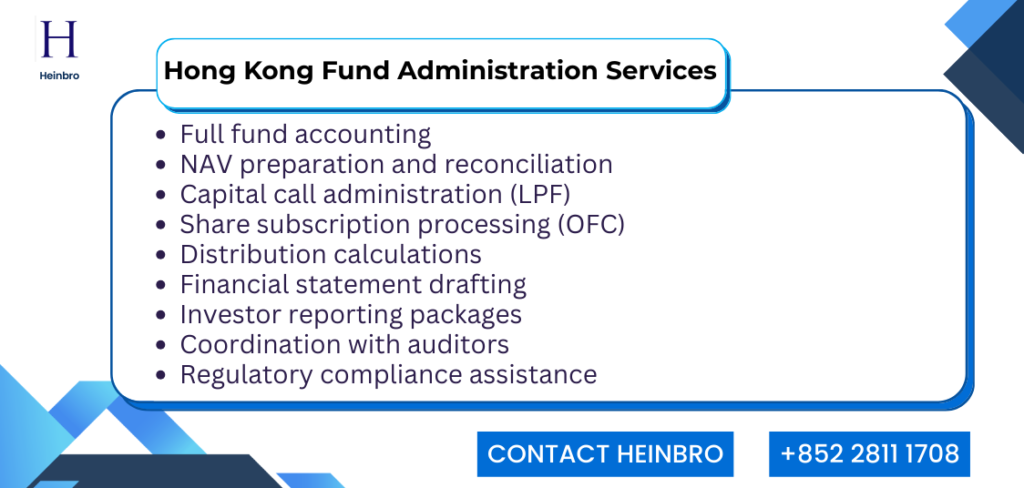

Outsourcing Fund Administration in Hong Kong

Both LPF and OFC structures commonly outsource fund administration functions. However, the scope differs depending on the capital model.

Outsourcing private equity fund administration in Hong Kong offers:

- Cost efficiency versus building internal teams

- Access to specialized fund accounting expertise

- Independent NAV calculation

- Regulatory reporting support

- Scalable operational infrastructure

Scope of Hong Kong Fund Administration Services

Structuring and Administering Hong Kong Private Equity Funds

Hong Kong private equity fund administration is directly shaped by the chosen fund vehicle — LPF or OFC. While OFC provides a corporate structure suitable for certain strategies, the LPF regime has positioned Hong Kong as a competitive onshore private equity domicile.

Effective fund administration — covering NAV governance, SFC compliance, AML obligations, capital call management, and inspection readiness — is essential regardless of structure.

For managers establishing or operating LPF or OFC structures in Hong Kong, Heinbro provides integrated regulatory and operational support. Heinbro assists with:

- Fund establishment (licensing and immigration support)

- Ongoing operations (compliance, inspection support, training)

- Business growth (recruitment and resourcing solutions)

With a strong understanding of Hong Kong’s SFC regulatory framework and fund operational realities, Heinbro supports private equity managers in building compliant, inspection-ready, and scalable fund administration structures. To book a free consultation, email Heinbro at heinbro@heinbro.com or contact us by phone at +852 2811 1708.